Stocks Camp Out Near Highs Before CPI with Oil Up

Published as of: August 11, 2026, 9:09 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 7,753.11 | -4.53 | -0.06% |

| Dow Jones Industrial Average® | 53,975.98 | -60.95 | -0.11% |

| Nasdaq Composite® | 26,605.36 | -85.26 | -0.32% |

| 10-year Treasury yield | 4.69% | Unch | -- |

| U.S. Dollar Index | 99.83 | +0.02 | +0.02% |

| Cboe Volatility Index® | 15.54 | +0.08 | +0.52% |

| WTI Crude Oil | $82.59 | +$0.45 | +0.55% |

| Bitcoin | $64,430 | +$310 | +0.48% |

(Tuesday market open) Today's early hours felt like a repeat of Monday courtesy of higher crude oil and relatively flat stock trading near last week's record highs. The dog days of summer are here, characterized by thin volume, narrow index moves, and a lighter earnings flow, while market participants cast a wary eye on Treasury yields that keep tightening the vise.

Today could see muted trading ahead of tomorrow's 8:30 a.m. ET July Consumer Price Index (CPI). Earnings from AI-related firms this afternoon including CoreWeave (CRWV) could lend the tech sector direction before Cisco's (CSCO) results tomorrow. Crude came off early peaks as Bloomberg reported progress toward a peace arrangement, citing Pakistan's defense minister, though traffic through the contested Strait of Hormuz remained extremely thin.

Crude and yields stalled Wall Street's parade Monday, sending the broader market down for the third session in the last four, while softness in Apple (AAPL) and Nvidia (NVDA) kept tech at bay. Several Treasury auctions could give clues about demand for U.S. debt, starting with 3-year notes today. Poor results might suggest loftier yields ahead, perhaps putting more pressure on stocks when the 30-year yield is already near 20-year highs.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

Three things to watch

- CPI growth seen light, but Fed on watch: Early expectations are for a 0.1% monthly rise in July CPI and a 0.2% core CPI gain, extracting food and energy. Annually, analysts expect 3.4% headline and 2.5% core, below June's 3.5% and 2.6%. While unpleasant surprises can't be ruled out—especially considering a producer price surge earlier this year—if numbers come in as expected it could reduce September hike odds. As of this morning, chances of a 25-basis point hike stood close to 50%, according to the CME FedWatch Tool, down from around 58% a week ago but up from last Friday's lows that followed the anemic July jobs report. "Last week's jobs report allows the Fed to be patient, but a hot CPI print this week would likely reverse that," said Collin Martin, head of fixed income research and strategy at the Schwab Center for Financial Research (SCFR). "When the labor market is strong and inflation is high, it's harder to defend not hiking rates. But if the labor market is showing weakness, there could be officials worried about potential downside risks following a rate hike."

- Earnings schedule eases, with optics on AI: Turning to earnings, the calendar might bring a welcome sense of rest after the last few exhausting weeks. Cisco is a key report often seen as a tech industry barometer. Its results follow CoreWeave and optics and laser maker Lumentum (LITE) later today before retailers begin their reporting season next week. Shares of Lumentum are up around 100% year to date, helped by growing optimism around the AI infrastructure space, though it did run into a buzz saw of pre-earnings selling Monday. The consensus earnings per share estimate is $2.97 on expected revenue of $987.9 million. Last time out, Lumentum beat analysts' earnings and revenue estimates, though not dramatically. CoreWeave has rallied lately after a summer swoon, lifted by several partnership announcements, which investors may want more color on. Nebius (NBIS), an AI infrastructure provider, also reports tomorrow with possible implications for Nvidia, which owns a nearly 10% stake in Nebius.

- Schwab clients stayed bullish in July: The Schwab Trading Activity Index™ (STAX) edged up to 59.80 in July from 59.12 in June, the highest reading since early 2022. Clients remained net buyers, with "dip buying" still a feature. Schwab clients tracked by STAX were net buyers by a two-to-one ratio, suggesting bullish sentiment remained firm, especially among self-directed traders. While major indices posted strong gains in July, those gains masked the fact that many individual stocks performed unevenly. While some stocks rose sharply, others struggled. In response, Schwab clients were selective about where they put their money, buying stocks that had pulled back and taking profits in names that had already run up or no longer offered the most compelling opportunities. Popular names bought by Schwab clients included SpaceX (SPCX), Micron (MU), Intel (INTC), Oracle (ORCL), and Tesla (TSLA). Names net sold by Schwab clients included Apple, Advanced Micro Devices (AMD), Broadcom (AVGO), PayPal (PYPL), and Adobe (ADBE).

On the move

- Rocket Lab (RKLB) slipped more than 4% after quarterly losses were wider than Wall Street had expected. Revenue topped estimates, however, rising 62% annually.

- Firms supporting the AI buildout made light gains early, including ASML (ASML) up nearly 3% and Super Micro Computer (SMCI) up 2.3%. Applied Materials (AMAT) rose 2% as well. SMCI reports earnings this afternoon and Applied Materials steps to the plate Thursday.

- Hims & Hers Health (HIMS) tumbled 7% ahead of the open after the telehealth platform reported much wider-than-expected quarterly losses. However, it does expect third-quarter revenue well above Wall Street's thinking. Revenue rose 38% year-over-year in its latest quarter.

- Intel (INTC) fell 1% early after its share sale offering announced Monday expanded to $20 billion from the original $15 billion. The proceeds are to fund its chip contract manufacturing business, Reuters reported.

- Conoco (COP), Chevron (CVX), and ExxonMobil (XOM) all climbed more than 4% Monday as oil rebounded.

- Coherent (COHR), another manufacturer of optical materials and semiconductors that reports Wednesday afternoon following Lumentum, fell 14% Monday, possibly driven by pre-earnings profit taking.

- Chip stocks mainly fell Monday while software mostly gained, continuing their divergence. Adobe (ADBE), Salesforce (CRM), and ServiceNow (NOW) rose, but Nvidia (NVDA) dropped nearly 3%. This came after the Financial Times reported Nvidia had reached a deal with several large Wall Street firms to help raise $500 billion to fund the AI buildout. Nvidia rebounded more than 1.6% early today.

- The S&P health care sector rose more than 1% Monday to fresh all-time highs, led by Eli Lilly (LLY). That stock appeared to draw strength from solid earnings reported last week showing firm weight loss and diabetes drug demand.

- The S&P 500 Index (SPX) traded in its narrowest intraday range of the year Monday, a sign of the featureless trading that often characterizes late summer. Volume fell below normal.

More insights from Schwab

Concentration risks abound but diversification possible: Broad global equity indexes are more concentrated due to an increased weight of the info tech and communication services sectors and recent capital investment related to AI. Even so, investors seeking diversification can find ways even in this era, our experts explained in a new look at international trends.

A closer look at inflation data: All eyes will be on this week's CPI and PPI numbers, especially in light of last week's jobs surprise. June presented evidence of slowing inflation, but was this only a one-time thing? Reporting in our biweekly Inflation Monitor digs into the data.

Inflation and small businesses: Today's NFIB Small Business Optimism Index and tomorrow's CPI could give investors a better look at how the inflation outlook is affecting small business confidence, said Kevin Gordon, head of macro research and strategy at SCFR, in his Week Ahead video.

Bond strategy considerations: Bond markets can shift quickly due to several factors. Our latest explainer shares how fixed income outcomes can change—and when to think about an active versus passive approach.

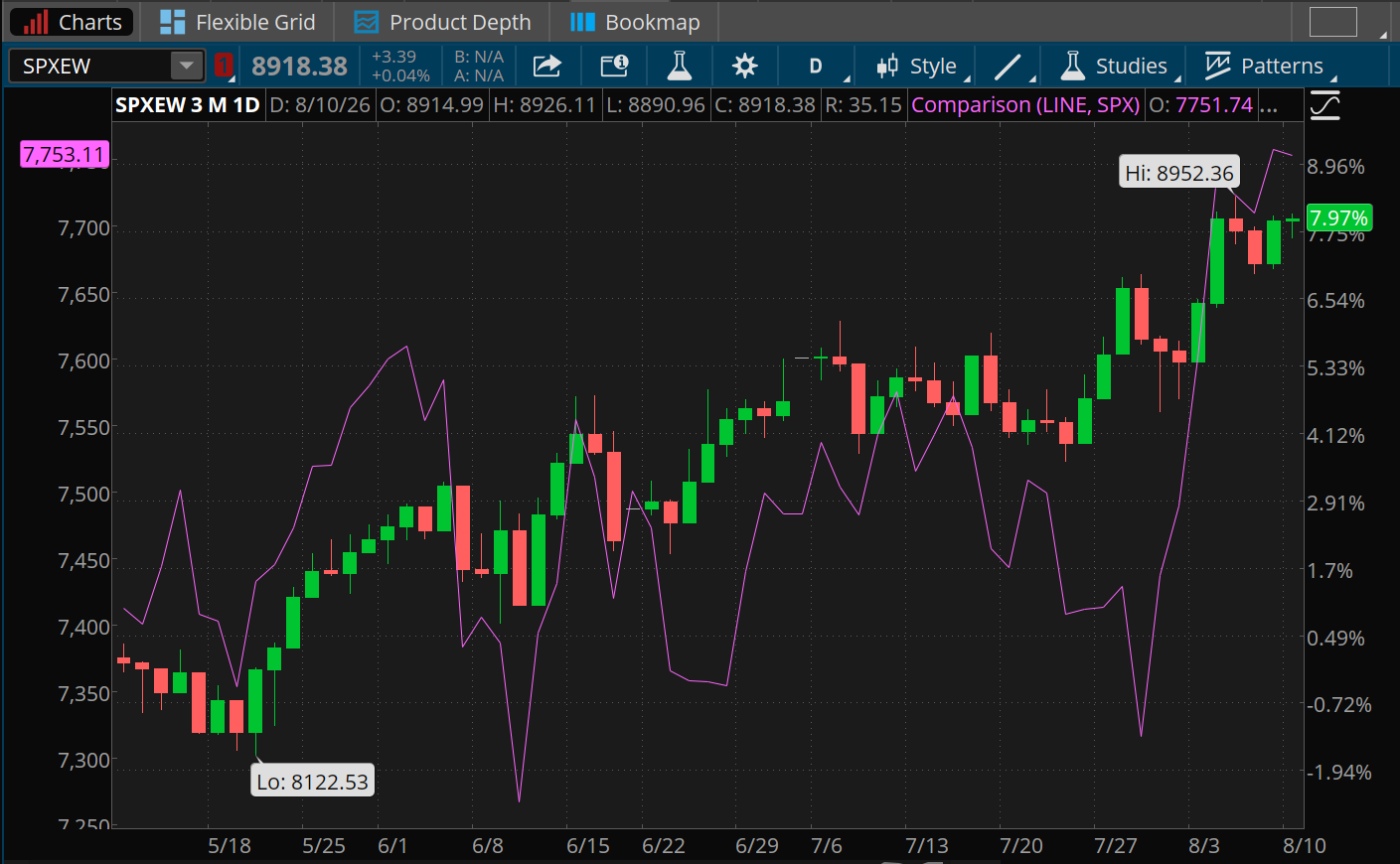

Chart of the day

Data source: S&P Dow Jones Indices. Chart source: thinkorswim® platform.

Past performance is no guarantee of future results.

For illustrative purposes only.

Since early April, the S&P 500 Index (SPX—purple line) and the S&P 500 Equal Weight Index (SPXEW—candlesticks) keep trading leadership. Between early April and late July, the equal weight index that weighs all components the same rather than by market weight was way ahead of the SPX, a sign of broadening interest in stocks outside the Magnificent Seven. However, the last two weeks saw the SPX pull ahead in a huge comeback as the SPXEW flattened, a sign of tech's major rebound and strength in stocks like Nvidia and Apple lately.

The week ahead

Check out the investors' calendar for a summary of the top economic events and earnings reports on tap this week.

August 12: July Consumer Price Index (CPI) and core CPI, and expected earnings from Nebius Group (NBIS), Cisco (CSCO), and Cerebras Systems (CBRS).

August 13: July Producer Price Index (PPI) and core PPI and expected earnings from Brookfield (BN), NetEase (NTES), JD.com (JD), Tapestry (TPR), Applied Materials (AMAT), and Nu Holdings (NU).

August 14: University of Michigan preliminary August consumer sentiment.

August 17: No major earnings or data expected.

August 18: July housing starts and building permits, July industrial production, and expected earnings from Home Depot (HD), Baidu (BIDU), and Toll Brothers (TOL).