Truce in Iran: Relief but Not Resolution

Key takeaways

- Markets rallied on the U.S. and Iran ceasefire announcement, but these moves look to be driven more by rapid unwinds of hedges and speculative positioning than by a fundamental resolution of the conflict. Market volatility is likely to remain high with headline risk driving short-term swings.

- Key signposts include whether the truce holds and how quickly (and under what conditions) traffic through the Strait of Hormuz and damaged energy infrastructure can normalize; both could keep energy prices elevated even if the war ends quickly.

- Downside to economic growth and upside to inflation effects can linger, even after the war ends. We continue to track this conflict and offer several possible scenarios, but currently see our Moderate and Severe scenarios as most likely with uncertainty remaining high. We do not view this as a moment to aggressively add risk.

Global markets staged a classic relief rally on news of a temporary truce in the U.S.-Israeli War in Iran. Global stock markets rallied, led by energy-reliant sectors and countries, while oil prices and bond yields dropped sharply. The immediate market response was a direct counter to the prevailing trends in place since the start of the war, reflecting the degree to which speculative positioning had shifted, and investor sentiment deteriorated.

Since the war started, several interrelated trends built up over the month of March that have served as "dry tinder" for a relief rally:

- Spiking energy prices: Global oil and gas prices have remained elevated with the Strait of Hormuz closed. The oil futures curve in steep backwardation (nearer-term, or "front month delivery contracts," considerably higher than later months) reflects physical demand for oil as well as investor speculation.

- Rising bond yields: Surging commodity prices have raised inflation concerns, quickly erasing expectations for the rate cuts that had been expected prior to the start of the war, likely leading to interest rates moving higher globally.

- Falling equity markets: The MSCI ACWI ex US Index fell by more than 10% in the month of March while the S&P 500 was down 5%. While not severe, the five-week consecutive drop for the S&P 500 has only happened twice in the last 15 years (2022 and 2011).

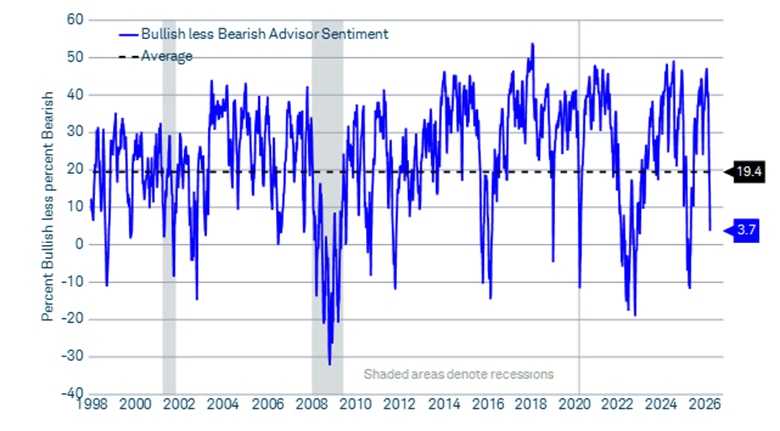

- Weakening investor sentiment: While there have been few signs of panic across global markets, rising risks related to the war-eroded investor sentiment are causing sustained pressure on risk assets (see chart below).

- Hedge fund short positioning had reportedly increased: Several broker-dealers reported large short-covering moves when the truce was announced, following a buildup of short positioning by hedge funds. Such "short-covering rallies" can be sharp, even if brief.

Investment Advisor Bull-Bear Sentiment dropped into bearish territory

Source: Charles Schwab, Macrobond, Investor Intelligence Survey on investment advisor investment sentiment as of 4/8/2026.

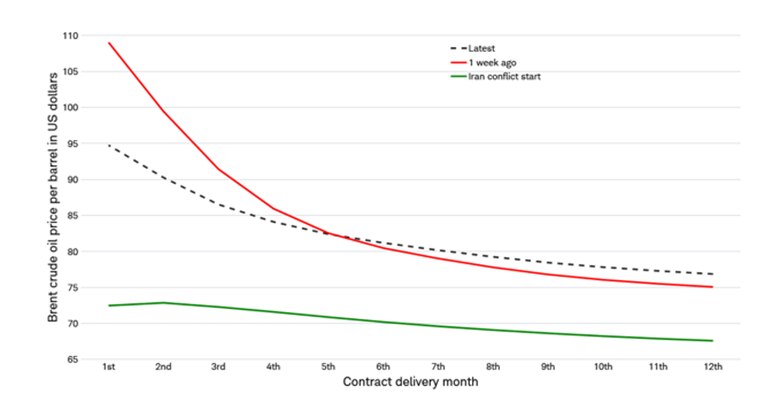

The Brent oil futures curve steepened sharply since the war but moderated post-truce

Source: Charles Schwab, Macrobond, Intercontinental Exchange, CME Group, as of 4/9/2026.

The oil futures curve shows where oil prices are today for different future delivery contract months; the curve's shape is influenced by supply, demand, and investment trends.

Brent is the leading global price benchmark for Atlantic basin crude oils. Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions. Futures and futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options [https://www.schwab.com/Futures_RiskDisclosure] prior to trading futures products. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Relief but not resolution

We view the immediate market reaction to the truce announcement as mostly about rapid unwinds of speculative positioning and hedges related to the war and less about a fundamental reassessment of the conflict and its implications. While news of a truce is certainly welcome—and does reduce near-term risks that could push energy prices higher that lead to worsening economic impacts—many questions remain about the ultimate outcome of the war.

First, and most immediate, is whether the truce will hold up. A two‑week pause lowers the probability of immediate escalation, but such arrangements can prove fragile, particularly when key strategic issues remain unresolved.

Second, there is still uncertainty around the reopening of the Strait of Hormuz. It's unclear currently whether, to what degree, and under what conditions the strait reopens, even if deescalation continues:

- Iran may seek to extract economic or political concessions in exchange for allowing tanker passage, which could prevent activity from normalizing and/or keep prices elevated.

- Incremental or conditional reopening could result in intermittent disruptions, use of convoys to facilitate passage, or insurance constraints that also restrict transport even if the strait is technically "open."

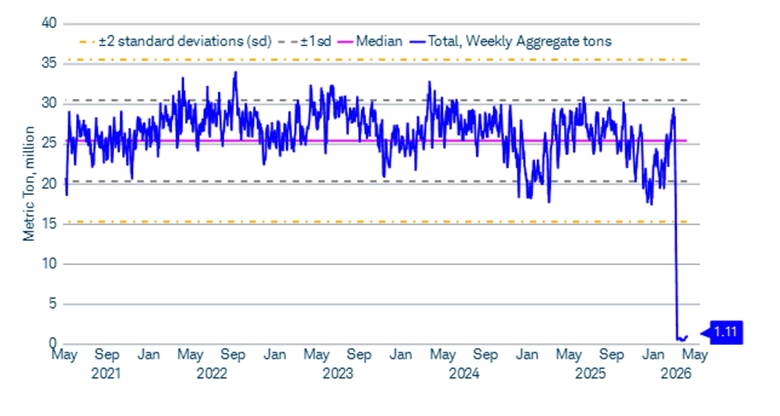

- Shipping insurers, charterers, and operators are likely to remain cautious, meaning commercial normalization may lag political agreements. Indeed, traffic through the strait remains virtually zero and will remain a key signpost for this crisis (see chart below).

Weekly trade volume through the Strait of Hormuz is unlikely to quickly recover

Source: Charles Schwab, International Monetary Fund, as of 4/8/2026.

Standard deviation measures the variation of data around an arithmetic average; a low standard deviation indicates that variation tends to be close to the average, while a high standard deviation indicates that the values are spread out over a wider range.

Third, physical damage to regional energy infrastructure has been significant. Even if the truce holds and military activity winds down, the restart of production and exports will take time because of the following realities:

- Damage to liquified natural gas (LNG) facilities, energy production and exploration activities, and refining capacity may take months, or longer, to come back online.

- Engineering constraints mean energy production restarts are often drawn out, with risks to equipment integrity if operations resume too quickly.

- Storage capacity limits raise the risk that ongoing disruptions lead to longer production shutdowns, extending the supply shock beyond the duration of hostilities.

As a result, the flow of energy may remain constrained even if the truce holds, keeping upward pressure on prices and acting as a drag on macro and market conditions.

Revisiting our scenarios

The Iran war quickly evolved from a regional conflict into a global energy supply shock, with the Strait of Hormuz effectively blocked for the first time since the 1970s. Global energy shocks historically have tended to result in more severe economic and financial market impacts versus other geopolitical conflicts. Year-to-date, the surge in oil prices is the largest in over 40 years, based on CME Group data.

Since the start of the Iran war, we have been tracking potential economic and market outcomes via a scenario analysis that includes different potential outcomes. The scenario table below provides an updated assessment of the likelihood of each case, and assumptions for the potential economic, policy, and market impacts. This analysis remains focused on the degree and duration of global energy supply disruptions. The longer energy and commodity supplies are constrained, the greater the economic damage.

- Upside: The likelihood of the upside case, defined by an imminent end to military operations and no lasting impacts to global growth, appears low due to the cumulative impact of lower energy production, energy infrastructure damage and time to recover to prior levels of production. This is the case even if the war was to end today.

- Moderate: The moderate case remains possible at this time, defined by a sustained wind down in military operations and a gradual normalization of energy flows. Oil prices may remain elevated through the second quarter due to the cumulative supply impact. Global growth and inflation are moderately impacted, with Asia and Europe most vulnerable.

- Adverse: In the adverse case, which we see as also possible today, military operations fade, but limited strikes may continue that impede the flow of traffic through the strait and to continue to impair and shutter the global energy infrastructure. This could keep energy prices elevated into the second half of 2026. The risk in the adverse case is economic stagnation in Europe and Asia due to larger dependencies on energy imports from the Middle East, as well as a weakening of U.S growth. Central banks, particularly in Europe, may be inclined to hike rates due to a spike in inflation.

- Severe: The severe case represents a possible scenario that could result in a global recession due to a prolonged conflict leading to acute energy and commodity shortages that drive overall inflation higher and leads to sharply tighter financial conditions. The combination of recession risk and higher inflation is a particularly difficult mix for policymakers to respond to. In this scenario, the potential for deeper and more persistent drawdowns across global equities increases.

Even if the war ends quickly, an energy shock has the potential for lingering impacts. How quickly production can return depends on the type of energy supply, amount of production curtailed and extent of infrastructure damage. The longer energy is unable to be exported, the greater the chance of complete energy production shutdowns. There is a non-linear impact of production halts for engineering reasons: for example, on the LNG side, there is a slow process of restarting production to avoid thermal shock to sub-zero cryogenic equipment.

Potential outcomes for the Iran war

| Scenario | Likelihood | Description | Oil Price (Brent) | Macro & Policy | Financial Market Impact |

|---|---|---|---|---|---|

| Upside: Imminent end with no impact to growth | Low | Military operations end; Middle East security stable | Price retreats below $75 | No lasting impacts to global growth; inflation proves transient; no major policy changes | Risk assets rebound led by the most impacted markets (Europe & Asia); bond yields drop on easing bias |

| Moderate:Gradual end to conflict, Contained impact | Medium | Military operations wind down; limited strikes may continue; energy flows gradually normalize | Eases to $75-100 range through 2Q | Differing local impacts to growth & inflation; slight impact to U.S. growth & inflation | Financial conditions remain tighter vs pre-war but no major corrections to broad markets; yields elevated but range-bound |

| Adverse:Gradual end but material macro & market impacts | Medium | Major military operations fade but strikes continue; energy supplies remain impaired | Stays in the $100-125 range into 2H | EU & Asia economic stagnation; U.S. weakens slightly via financial conditions; monetary tightening bias; limited fiscal response | Broad financial condition tightening; equities correct further; credit spreads widen modestly; bond yields rise further on inflation and rate hike concerns |

| Severe:Prolonged Conflict (>6 months) | Low | Military operations continue; global commodity shock propagates | Exceeds $125; volatility into 4Q | Global recession likely; severe financial condition tightening; broad fiscal + monetary policy toolkits utilized | Global equity bear market; credit stress propagates; classic flight to safety; bond yields could rise if stagflation takes hold |

The physical supply of energy is a critical signpost. The war has effectively stopped all traffic from moving through the Strait of Hormuz (as described in our chart above). It's not just energy that is disrupted here—4.5% of annual global trade also passes through the Strait, according to Bloomberg estimates. Fertilizer, helium for semiconductor chip production, precious metals, aluminum, cement, and naphtha for plastic production, are some of the major commodities at risk here.

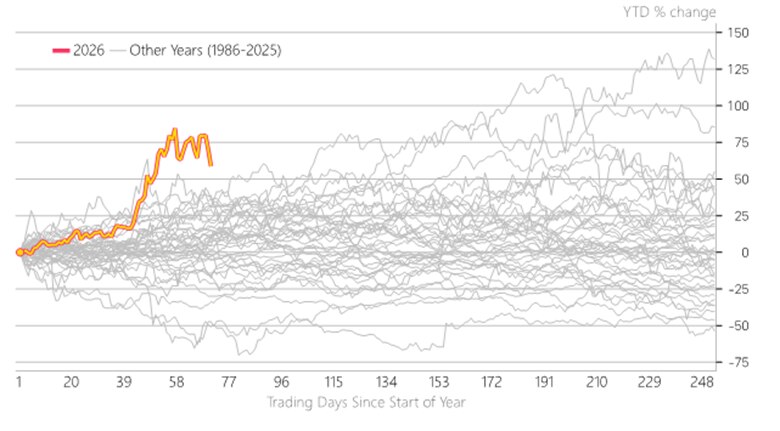

Oil prices, while down from the peak seen in late March, have increased this year at a rate not seen in over 40 years (see chart below). For prices to retreat materially further from here, we would likely need to see not only a more permanent peace agreement emerge, but also a steady normalization of energy production and shipping.

Brent crude year-to-date percent price change by calendar year

Source: Charles Schwab, Macrobond, Intercontinental Exchange, CME Group, as of 4/8/2026, using available daily data back to 1986.

The chart shows the progression of oil prices over all trading days for each year we have daily data to exhibit the severity of this year's price rise.

Brent is the leading global price benchmark for Atlantic basin crude oils. Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

In sum

The temporary truce is welcome news and does remove near-term risks associated with intensifying military operations and strikes on energy infrastructure, but many critical questions are still unanswered and the possibility for a wide range of potential outcomes remains. We reiterate our view that now is not the time to aggressively add risk. Without more clarity on the fundamental impacts of the U.S.-Israeli War in Iran, market volatility is apt to remain elevated with potential for short, but sharp swings driven by headline risk.

Heather O'Leary, Senior Manager, Equity Research and Strategy, contributed to this report.