How Do Treasury Auctions Work?

Key takeaways

- Treasury auctions are how the U.S. government borrows money—selling bills, notes, and bonds to investors and setting yields in the process.

- Most Treasuries are marketable securities, meaning they can be bought at auction and later traded in the secondary market.

- Auction results matter more when government debt levels are rising and interest rates are elevated, because demand can influence yields and ripple through markets and the broader economy.

- Bidders can offer non-competitive bids (accepting the yield set at auction) or competitive bids (naming the yield they're willing to accept), but all successful bidders of either type are awarded the same highest accepted yield.

- To gauge Treasury demand, investors can monitor measures like the bid-to-cover ratio, the tail, and how much government debt primary dealers must absorb.

At their core, U.S. Treasury auctions aren't all that different from other public or private auctions. Buyers and sellers evaluate what's up for sale and haggle over prices until they agree.

The only difference between auctioning a bike, house, or newly issued Treasury bill or note is that the latter typically involves billions of dollars and can move global markets.

Since its founding, the United States has used debt to help pay for the services it provides. The government still offers a range of securities today, such as Treasury bonds, notes, and bills, also known as T-bonds, T-notes, and T-bills. These instruments vary by factors like maturity length, offering size, interest payment schedule, and amount of interest paid. The last factor determines the return, or yield, an investor receives every year.

Most Treasuries are known as marketable securities. This means after they're sold by the government through Treasury auctions—where individual investors can buy them—they can be resold in the secondary market. Banks and brokers also buy securities at these auctions and then resell them to the public. Non-marketable securities, such as savings bonds, can't be resold.

The Treasury typically holds more than 400 auctions each year and sold roughly $29.7 trillion worth of marketable securities in 2025, according to U.S. government data. Interest rates are set at these auctions and affect the prices people, banks, and brokers pay the Treasury for the security.

Until recently, these regularly scheduled sales of government debt were generally background noise on Wall Street. But they've become more relevant of late with government debt rising substantially and interest rates remaining elevated.

Higher Treasury yields have attracted some new investors, while occasional signs of sluggish auction demand have sparked market volatility, forcing market watchers to pay closer attention to these once under-the-radar events. All of this means it's worth learning how Treasury auctions work, who and what they involve, and why they matter.

How Treasury auctions work

Each quarter, the U.S. Treasury Department releases refunding announcements estimating how much debt will be auctioned in the next two quarters and how that debt will be split into various maturities. If the Treasury forecasts it needs to issue more debt than expected, it can cause yields to climb.

Like the auctions themselves, refunding announcements used to be ignored by most investors but now they draw far more attention. That's because they outline increasing amounts of government debt after major spending increases during and following the pandemic. This has raised concerns that investors might demand higher yields, which could drive up borrowing costs and weigh on stock prices.

The amount of debt auctioned generally reflects how much money the Treasury needs to keep the government running. While Congress decides how much to spend in its appropriations process, the revenues the government earns aren't always consistent. And because the government spends more than it takes in each year, it can't spend money without borrowing. Those who buy the debt at the auctions supply the government with extra money it needs, but they don't do it for free. That's where yields come in.

The Treasury pays investors for buying its debt, usually in fixed payments every six months (see more below). That's the enticement for holding the debt. Investors can choose to buy debt that matures in time frames ranging from four weeks to 30 years.

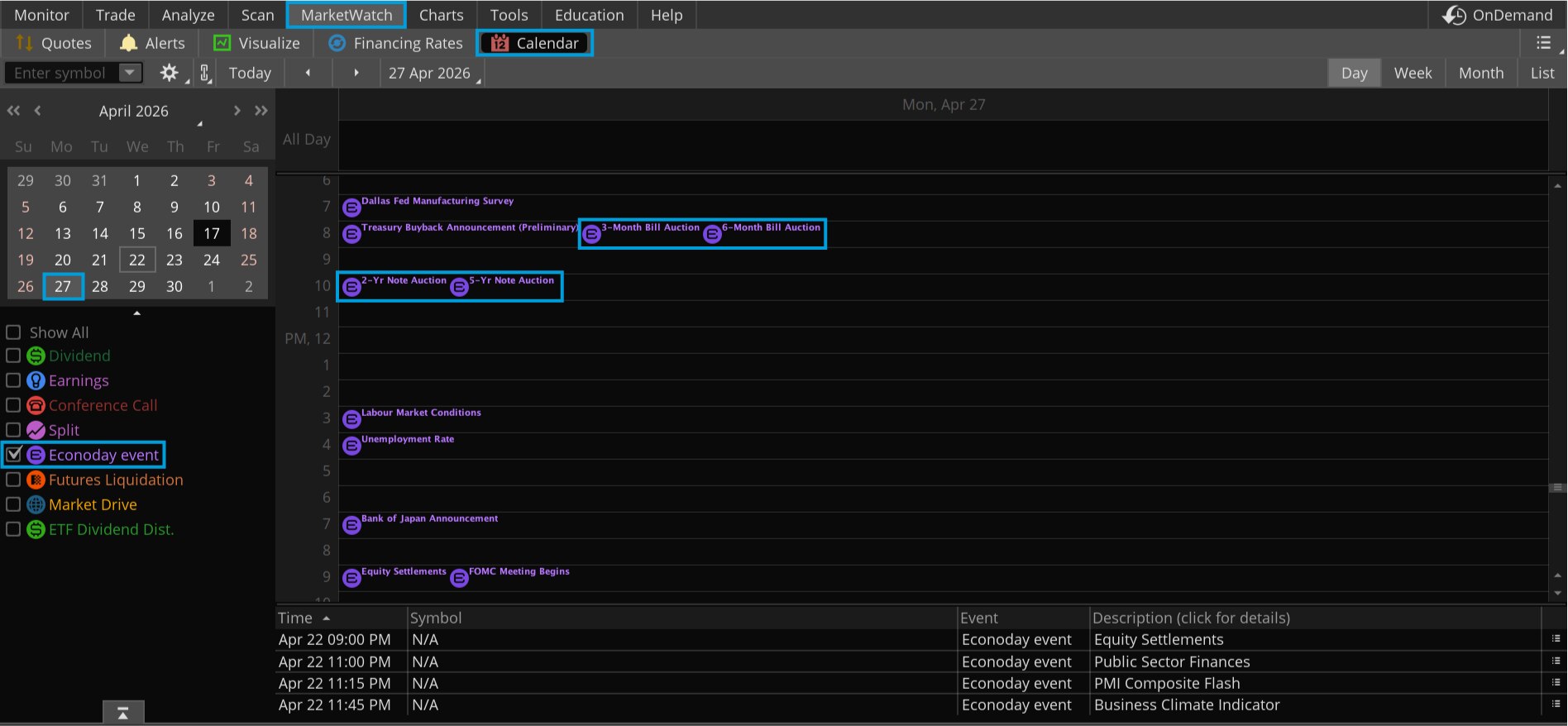

Where to find the auction calendar

U.S. debt is issued through auctions held by the U.S. Treasury. You can find its schedule of announcements and auction dates on the thinkorswim® platform. From the MarketWatch tab, select Calendar, the date in question, and uncheck all boxes except Econoday event to reveal the time and auction lineup for that day.

Source: thinkorswim platform

For illustrative purposes only.

In addition to thinkorswim, the Treasury's website features a tentative auction schedule. The announcement date is typically a day or two before the auction, and the settlement date usually comes several days after the auction.

Investors can also sign up for the Treasury's mailing list to get regular emails with auction dates.

The Treasury's auction calendar details the securities being offered, the amounts, the auction date, issue date, and maturity date, as well as the closing times for competitive and non-competitive bidding. The government sells most short-term Treasury bills weekly, while Treasury notes and bonds, which have longer maturities, are auctioned less often.

What's for sale at Treasury auctions?

The government auctions its debt in various forms, most commonly in the form of Treasury bills. These bills range in duration from four weeks to one year. Less often, the government will auction Treasury notes with maturities from two to 10 years and Treasury bonds with maturities of 20 to 30 years. The yields on these bills, notes, and bonds are fixed, meaning they pay the same rate throughout the lifespan of the contract.

A less common auction is for TIPS, or Treasury Inflation-Protected Securities. These have maturities of five, 10, or 30 years and are designed to help protect investors against inflation. Their principal values can rise (or fall) over time, depending on the inflation rate.

Another offering is Floating Rate Notes (FRN), which are relatively short-term investments that mature in two years and have an interest rate that can change (or "float") over time.

Who buys Treasuries at auction?

There are many types of buyers at Treasury auctions. Individual investors, institutional investors (such as banks), and foreign central banks all line up. Anyone can bid for Treasuries through a TreasuryDirect account or through a bank, broker, or dealer.

Schwab also offers Treasuries through the secondary market, where market participants trade Treasuries that have already been issued or purchased at auctions.

Schwab clients can participate in Treasury auctions on Schwab.com. From the Trade tab, select Bonds. The Invest in Bonds at Schwab page will automatically appear. Scroll down and select the Treasury Auctions link located under the list of fixed income offerings. Investors who choose to participate will be prompted to enter order details, such as dollar amount and order type.

For additional information on how to buy Treasuries at Schwab, watch this video to see an example of how the process works.

How Treasury auction bidding works

At the auction, the Treasury first accepts all non-competitive bids, or those in which the bidder—which can be individuals, partnerships, corporations, foreign monetary authorities, and others—agrees to accept the rate, yield, or discount margin determined at the auction. Then it accepts competitive bids until the entire amount of the offering is awarded. A competitive bid means investors specify the rate, yield, or discount margin they're willing to accept. All successful bidders get the same rate, yield, or discount margin as the highest accepted bid.

"Yields at an auction will generally be quite close to the yield of issues within the secondary market, usually within a basis point or two," said Collin Martin, director of fixed income strategy at the Schwab Center for Financial Research. "An auction that was, say, five basis points away would be a huge gap."

What's the score?

The end of a Treasury auction, like the end of a game, comes with its own version of a box score. There are a few terms that show up in the results that investors should know.

- Bid-to-cover ratio: Measures demand at the auction by comparing the number of bids received relative to the amount of Treasuries being auctioned. A higher ratio generally suggests stronger demand.

- The tail: Measures the difference between the yield awarded at auction and the yield implied by pre-auction trading. A positive tail can indicate weak auction demand that required the government to offer a higher yield to attract buyers. This can cause Treasury yields to rise when the results of the auction are released.

- Primary dealers: Measures the percentage of debt bought by primary dealers, who buy the portion of the offering not purchased by other investors. A high percentage here can also indicate weak auction demand.

The Treasury Department regularly publishes auction results on its site and lets investors look back at recent history to see what each one yielded.

Potential risks of Treasury debt

Why do banks and investors buy Treasury debt? Fixed income investments generate income and help provide capital preservation, along with portfolio diversification. U.S. Treasuries are backed with the full faith and credit of the U.S. government, meaning they're often considered low-risk investments.

However, no investment is without risk. U.S. Treasuries often don't pay yields as high as riskier corporate or municipal bonds, and prices can fluctuate in the secondary market like any investment.

Still, the United States has never defaulted on its debt, and the U.S. dollar remains the world's primary reserve currency. As a result, U.S. Treasury auctions continue to attract both domestic and foreign buyers.

Bottom line: Why Treasury auctions matter

For investors, watching Treasury auctions is essential, even if buying a bill, note, or bond isn't the primary goal. These auctions act as a real-time gauge of demand for U.S. government debt, which influences Treasury yields and, by extension, financial markets and the broader economy.

By monitoring Treasury auction results, investors can make more informed decisions and manage risks with more confidence.