What’s Next for Emerging-Market Bonds?

Our view on emerging-market bonds is less optimistic after Federal Reserve policymakers indicated in mid-June that they may raise short-term interest rates sooner than previously expected. Although we had previously suggested investors consider overweighting emerging-market (EM) bonds relative to a benchmark target allocation, we now have a neutral view on EM bonds.

For emerging-market bonds, a Fed policy change would be a potentially seismic event. For the past year, accommodative Fed policy, the relatively high yields that emerging-market (EM) bonds offered, a weaker U.S. dollar, and the improvement in global growth and trade all supported a positive view of EM bonds. However, a shift toward tighter Fed policy could lead to slower global growth, a stronger dollar, and less appetite for risk among investors—all negatives for EM bonds.

The changing landscape for EM bonds

At the start of the COVID-19 pandemic, the Fed rushed to provide emergency programs to support the flow of credit—lowering interest rates and increasing dollar liquidity to the global markets. The expansionary monetary policy in the U.S. jumpstarted investors’ risk appetite. This appetite, paired with the rebound in global growth and higher yields in EM markets, made emerging-market bonds look attractive.

Recently however, things have started to change. The Federal Reserve released its quarterly projections for the federal funds rate, known as the dot plot, on June 16th. The median projection from Fed participants now points to two rate hikes in 2023, a more hawkish projection than in March.

Meanwhile, China—the largest issuer of debt in the EM bond market—has been pushing harder on the brakes for new credit growth throughout Q2. These changes point to the likelihood of slower long-term growth, a stronger U.S. dollar, and reduced investor appetite for risk.

Consequently, our new view on EM bonds is based on the prospect for higher U.S. yields, tighter Federal Reserve policy, weaker commodity prices, and China’s declining credit growth. Let’s look more closely at each.

1. Higher U.S. Treasury yields are expected

We expect the 10-year Treasury yield to rise to over 2% by the end of the year. This makes emerging-market bonds look less attractive from an interest-rate sensitivity perspective (also known as duration). Due to strong investor appetite for risk, emerging-market issuers have been able to issue longer-term bonds in recent years. Consequently, the interest-rate sensitivity of EM bonds has increased from an average of 5.64 years throughout 2015 to 2018, to just shy of 7 years today.

Emerging-market bonds come with a high duration

Source: Bloomberg. USD EM Bonds = Bloomberg Barclays USD Emerging Market Bond Total Return Index Option Adjusted Duration (EMUSTRUU Index). LC EM Bonds = Local Currency Emerging Market Bond Total Return Option Adjusted Duration (EMLCTRUU Index). Daily data as of 6/25/2021.

This high duration makes EM bonds particularly susceptible to price declines when Treasury yields rise. The first quarter of 2021 provided a glimpse into that dynamic. EM bond total returns pulled back roughly 4% in Q1 when the U.S. 10-year Treasury yield reached as high as 1.7%. If our outlook for the 10-year yield to rise above 2% comes to fruition, EM bond prices likely would decline.

2. The Federal Reserve is moving toward tighter monetary policy

Emerging-market bonds are particularly sensitive to changes in Fed policy. The Federal Reserve’s June dot plot indicated a change from zero rate hikes in 2023 previously to two rate hikes in 2023. This hawkish tilt of the Fed implied slower global growth, a stronger dollar, and less appetite for risk among investors—all of which are negatives for EM bonds.

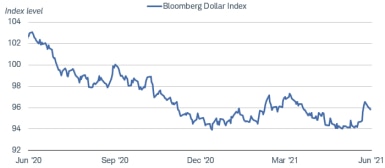

The value of the U.S. dollar has risen quickly

Source: Bloomberg. Bloomberg Dollar Index = Bloomberg Trade-Weighted Dollar Index (BBDX Index). Daily data as of 6/25/2021. Past performance is no guarantee of future results.

The rise in the dollar is particularly harmful for local-currency EM bonds. The coupon payments from local-currency bonds will now be worth less when converted back into U.S. dollars, driving down the value of the bonds to U.S. investors.

3. Commodity prices have dropped

Emerging-market bond performance is tied to commodity prices, because many issuing countries tend to be large exporters of commodities. When commodity prices fall, gross domestic product (GDP) growth in emerging-market economies tends to fall, as well. The recent spike in the dollar, paired with weakness in most commodities, does not bode well for the stability of emerging-market economies. Many emerging-market countries took on higher levels of debt and implemented unprecedentedly accommodative monetary policy throughout the pandemic. Therefore, the drop in commodity prices makes it even more challenging for EM countries given their increased debt load. Lower economic stability can translate to a higher risk of default, higher credit spreads, and lower EM bond prices.

4. China is hitting the brakes

The size of China’s economy and the amount of debt issued dwarfs the rest of the emerging-market debt universe. In fact, China is the highest weight in the Bloomberg Barclays Local Currency Emerging Market Bond Index, coming in at a whopping 46%. So, it should come as no surprise that when China makes a policy change, it flows through to the other EM economies. The Chinese government decided to let pandemic-related stimulus wane in Q4 last year. Over the past two months, the rate of credit growth in the Chinese economy has dropped off so quickly that it turned negative.

China’s credit impulse is dropping

Note: The credit impulse is the change in new credit issued as a proportion of GDP.

Source: Bloomberg. China’s Credit Impulse Growth Rate = Bloomberg Economics China Credit Impulse 12-Month Net Change (CHBGREVA Index). Monthly data as of May 2021.

This new phase of declining credit growth means less investment spending by China, leading to a decline in foreign direct investment and commodity purchases for other emerging-market countries. This slowdown could translate to marginally lower GDP growth and lower commodity prices for emerging markets, which weigh on EM bond performance.

What to consider now

We still believe investors with an appetite for risk can maintain an allocation to EM bonds, which we consider an “aggressive-income” asset class. However, there’s not much room for price appreciation given today’s yields.

We suggest investors:

- Consider keeping a neutral weighting to EM bonds based on an allocation target that is in line with their goals and investing time horizon, allocating no more than 20% of the portfolio to EM bonds.

- Use mutual funds or exchange-traded funds (ETFs) to get the benefit of broad diversification.

Please reach out to a Schwab Financial Consultant if you need assistance determining what is right for your unique circumstances and whether to invest in EM bonds.