VIX ETFs: The Facts and Risks

Investors often worry about market volatility—especially the kind of big negative moves seen during the credit crisis of 2008 or at the onset of the COVID-19 pandemic in early 2020. It's natural to look for investments that may increase in value when markets decline in order to get some downside protection, which is why some investors start looking toward the VIX®, a volatility index published by the Chicago Board Options Exchange.1 You can't buy the VIX itself, though, and the exchange-traded products that use VIX futures have some big risks that investors should understand before buying.

What is the VIX?

The name VIX is an abbreviation for "volatility index." Its actual calculation is complicated, but the basic goal is to measure how much volatility investors expect to see in the S&P 500® Index over the next 30 days, based on prices of S&P 500 Index options. When options traders think the stock market is likely to be calm, the VIX is low; when they expect big swings in the market, the VIX tends to go up.

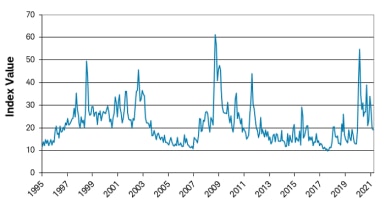

VIX index value over time

Source: CSIA calculation based on Morningstar Direct data, as of April 30, 2021.

During times of high market turmoil, the VIX has tended to rise. The chart above shows the VIX index moved steadily higher as the market approached the peak of the late 1990s technology bubble, calmed down during the steady growth period of 2003-2007, spiked during the 2008 credit crisis and in the latter half of 2011, and saw another large spike when the COVID-19 pandemic hit in early 2020. Because of this pattern of behavior, the VIX is sometimes referred to as the "fear index "—when market participants are worried about the market, the VIX tends to rise.

Investors who see the VIX having increased sharply while the market went down might be tempted to seek an investment in the VIX as a source of potential protection during market volatility.

Accessing the VIX through futures contracts

Like all indexes, the VIX is not something you can buy directly. Moreover, unlike a stock index such as the S&P 500, you can't even buy a basket of underlying components to mimic the VIX. Instead, the only way investors can access the VIX is through futures contracts and through exchange-traded funds (ETFs) and exchange-traded notes (ETNs) that own those futures contracts.

A futures contract is an agreement to deliver something at a certain point in the future, for a price that's agreed upon in the present. The first futures contracts were for commodities such as wheat and corn, and they're available for many commodities now, including oil and natural gas.

Index futures, such as those tied to the value of an index like the S&P 500 or the VIX, do not involve actual delivery of anything when the futures contract matures. Instead, they use a cash delivery tied to the value of the index on the delivery date.

The risks of VIX futures

The potential problem, as with any futures contract, is contango—that is, when the futures price for something is higher than its current price. For instance, if VIX is at 15 today, and a one-month VIX futures contract is trading at 16, then the VIX futures market is in contango.

Why is this a problem? Well, imagine that your goal is to always have a certain part of your portfolio invested in VIX futures. If the futures contracts are always more expensive than the current VIX level, then you pay a premium every time you buy futures. You're essentially buying high and selling low, which erodes the value of your investment over time.

VIX futures and contango in action

The contango problem isn't purely academic; VIX futures contracts have often been more expensive than the VIX index. According to Bloomberg, in 49 of the past 60 months dating back to April 2016, the three-month VIX futures contract was above the VIX level. You can see the effect in action in the chart below.

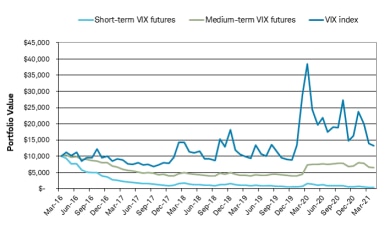

Value of $10,000 invested in VIX or VIX futures

Source: CSIA calculation based on Morningstar Direct data, as of April 30, 2021. The example is hypothetical and provided for illustrative purposes only.

In this figure, you can see what $10,000 would be worth if it had been invested in the VIX itself (which, as mentioned earlier, is impossible), a portfolio of short-term VIX futures contracts, or a portfolio of medium-term VIX futures contracts over the previous five years. These portfolios are based on actual exchange-traded funds that buy VIX futures contracts.

As you can see, the futures contracts have lagged significantly behind the value of the VIX index. By the end of the period, the value of $10,000 hypothetically invested in the VIX itself would have risen to over $13,000, while the portfolio of medium-term VIX futures contracts was worth under $7,000, and the short-term VIX futures contracts had fallen to under $500. Had an investor actually been able to buy the VIX, the investment would have made some money, but the actual investable instruments based on VIX (including ETFs and ETNs tied to those instruments) lost significant amounts of money.

Just because an investment has VIX in its name doesn't mean that it will move in line with the VIX Index. Furthermore, as the charts show, the VIX itself can be extremely volatile—the index lost 54% of its value between March 2020 and July 2020. Investors cannot buy VIX, and even if they could, it would be an investment with a great deal of risk.

1. The Chicago Board Options Exchange Volatility Index® (VIX®) reflects a market estimate of future volatility. VIX is constructed using the implied volatilities of a wide range of S&P 500 index options. This volatility is meant to be forward-looking and is calculated from both calls and puts.