Mysterious Ways: Bullish Sentiment Grows, With Positive Offsets

With less than two months left in what has been an extraordinary (and mystifying) year on multiple fronts, stocks have maintained a largely uninterrupted trek higher (at the index level) in the face of myriad headwinds—not least being the mid-year surge in the delta variant, supply chain disruptions on a global scale, surging energy prices, and an uncomfortable spike in inflation. While that laundry list of concerns ultimately led to the S&P 500’s 5.2% drawdown in September (the largest since November 2020), the drop was quickly erased in 13 days, as investors embraced the weakness and preserved confidence.

That unwavering conviction in risk assets has brought with it a sharp resurgence in stretched sentiment. Across several metrics—both attitudinal and behavioral—complacency looks to again be settling in. While not every indicator is flashing red, a handful have returned to zones in which they found themselves earlier this year, when euphoria was permeating multiple segments of the market.

Say what?

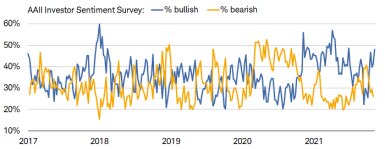

Starting in perhaps a relatively benign area, we’ll first look at attitudinal measures of sentiment—what investors are saying and thinking. Shown below is the AAII Investor Sentiment Survey, which simply asks respondents if they’re feeling bullish or bearish (illustrated by the blue and yellow lines). Over the past few weeks, there has been a sharp increase in bullishness, accompanied by an equally swift decrease in bearishness. For now, the good news is that the spread between the camps isn’t matching the massive divergence in April this year; and even at that time, the peak in confidence didn’t precede any major weakness for stocks.

Bears moving towards hibernation

Source: Charles Schwab, American Association of Individual Investors (AAII), Bloomberg, as of 11/11/2021.

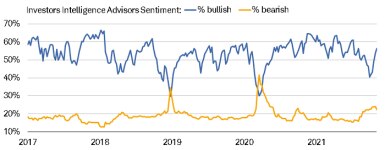

An uptick in bullishness can also be seen in the Investors Intelligence (II) Advisors Sentiment survey, which assesses more than a hundred investing newsletters to gauge authors’ views on the stock market. As shown below, bullish sentiment has increased sharply, but not yet to euphoric levels. Interestingly, both lines started to converge heading into October, consistent with prior major declines in the stock market (though not as sharp); yet that dip didn’t turn into a more severe correction.

Still some bears in the II crowd

Source: Charles Schwab, FactSet, as of 11/5/2021.

To behave or not to behave

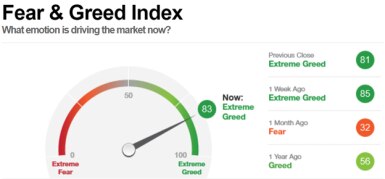

Moving onto the behavioral side—measuring actual positioning and what investors are doing with their money—we’ll first look at CNN’s Fear & Greed Index. As pointed out in the footnote below, this is an amalgamation of several indicators, including stocks’ momentum, demand for junk bonds, and market volatility, among others. As of November 12th, the index is flashing dark green, which indicates extreme greed. Perhaps most telling from this graphic is the swift move into greed territory, given it was in the fear zone just one month ago.

Fear to greed with speed

Source: CNN (https://money.cnn.com/data/fear-and-greed/), as of 11/12/2021. The CNN Fear and Greed Index examines seven different factors (stock price momentum, stock price strength, stock price breadth, put/call options, junk bond demand, market volatility, safe haven demand to establish how much fear and greed there is in the market.

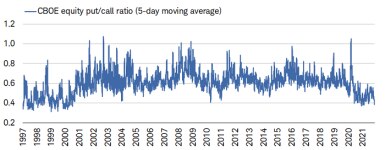

Zooming in on one of the indicators within the Fear & Greed Index, the CBOE put/call ratio measures equity put option purchases to call option purchases. As shown below, it has moved lower, indicating investors are buying more calls (bullish bets) than puts (bearish bets). The ratio has yet to return to its pre-pandemic zone on a sustained basis and remains near levels seen during the euphoric period of the late-1990s.

Put/call ratio hovering in a bullish zone

Source: Charles Schwab, Bloomberg, as of 11/15/2021.

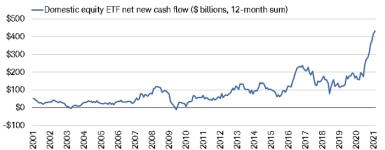

Another way to view equity market bets is by looking at flows into equity exchange-traded funds (ETFs). As shown below, investors have put more than $400 billion into domestic equity ETFs over the past year. That is by far a record sum and well exceeds the prior peaks in 2008-2009 and 2016-2017. This should be considered in the context of an increase in asset prices over time, as well as the comparatively weak flows during the prior year. Yet, it emphasizes that investors have embraced equities unashamedly since the pandemic began—perhaps unsurprising given the S&P 500 has more than doubled in less than two years.

Going with the flow

Source: Charles Schwab, Investment Company Institute (ICI), as of 9/30/2021.

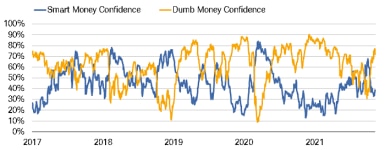

Fund flows (for mutual funds as well) are typically indicative of where “the crowd” is moving and are one of the inputs for SentimenTrader’s Dumb Money Confidence—which is shown in the next chart alongside Smart Money Confidence. Using SentimenTrader’s definitions, the “dumb money” tracks the positioning of smaller odd-lot traders and speculators, while the “smart money” tracks the positioning of large commercial hedgers and institutional traders.

As you can see below, Dumb Money Confidence has increased sharply over the past month and now sits in extreme optimism territory (above 70%). When we last penned an update on sentiment over the summer, confidence was in a similarly optimistic state; but the difference back then was that the “smart money” was following suit. The opposite is the case today, as Smart Money Confidence has plunged and is hovering near its lowest since August.

Smart Money and Dumb Money diverge

Source: Charles Schwab, SentimenTrader, as of 11/12/2021. SentimenTrader's Smart Money Confidence and Dumb Money Confidence Indexes are used to see what the “good” market timers are doing with their money compared to what the “bad” market timers are doing and are presented on a scale of 0% to 100%. When the Smart Money Confidence Index is at 100%, it means that those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. The Dumb Money Confidence Index works in the opposite manner.

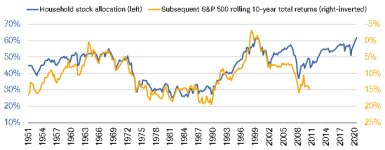

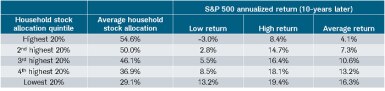

Among the most-watched behavioral measures of sentiment is households’ allocation to equities, shown by the blue line in the chart below. As you can see, at 62%, exposure is just shy of its all-time high in 2000, which preceded the tech bust. You can also see, shown by the yellow line, that there is a strong negative correlation to subsequent 10-year returns for the S&P 500—meaning that as exposure to equities increased, future performance weakened historically. A more detailed look can be seen in the accompanying table, which shows households’ allocations by quintile. When allocations were in the highest quintile historically—where they currently are—the average 10-year (annual) return was the lowest among all zones.

Households’ elevated exposure to equities

Source: Charles Schwab, Bloomberg, ©Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/., as of 6/30/2021. Equity allocation (includes mutual funds and pension funds) is % of total equites, bonds and cash. Past performance is no guarantee of future results.

In sum

As mentioned at the beginning of this report, not every sentiment indicator we track is currently flashing warning signals; some metrics have yet to suggest euphoria. With the market having recovered swiftly from its September-October weakness in the face of higher inflation, massive disruptions to the global supply chain, and a decelerating earnings growth rate; a persistent increase in bullish sentiment exposes some vulnerabilities for stocks. As we always like to remind investors, however, sentiment at extremes isn’t itself enough to suggest a contrarian move in stocks. A negative (or positive) catalyst is typically needed to tip the scales.

For now, strong market breadth and firm profit margins have acted as positive offsets to excessive optimism. Additionally, the market’s weakness under the surface has allowed several segments to reset, given 92% of stocks within the S&P 500 have already had a 10% correction from a high at some point this year; with the average drawdown being -18%. The average drawdown within the NASDAQ and Russell 2000 indexes is even greater, as shown below. As noted, though, the rotational nature of these corrections is such that rolling pockets of weakness have been offset by pockets of strength, which has kept the indexes’ declines more muted; and in turn, optimistic sentiment elevated.

The market’s massive churn

Source: Charles Schwab, Bloomberg, as of 11/12/2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Key to the market’s success moving forward will be continued strength in breadth and fundamentals. Earnings are still growing, but at a decreasing rate; and while companies’ profit margins are still benefiting from massive cuts to capital and labor last year—as well cost pass-through to customers—stellar growth will inevitably ease. We continue to recommend that investors focus on segments of the market with higher earnings revisions—with an overarching emphasis on high quality.