Moving in Stereo: Churn and Rotations Causing Swings in Sentiment

The stock market’s rally off the recent lows has been a welcome reprieve relative to the volatility-spiked pullback that began on “bleak Friday” alongside the COVID-19 omicron variant news. In keeping with ongoing rapid-fire rotations at the sector level, investor sentiment has been on a seesaw as well. In our 2022 outlook published at the end of November, we highlighted that sentiment was then in highly euphoric territory (a generally-contrarian signal).

We penned one of these sentiment-oriented biweekly reports in mid-November, which looked at several metrics that were then at opposite ends of the spectrum relative to where they are today. That mid-November level of complacency arguably laid some of the groundwork for the 4.4% pullback the S&P 500 experienced during the final week of November. That was slightly better than the 5.2% pullback that began on September 2 this year; but importantly, that was also preceded by lofty sentiment conditions.

With relatively muted index-level drawdowns year-to-date (YTD), sentiment swings have been a bit more dramatic. This may be partly explained by the much more significant stock-level drawdowns so far this year, as shown below. The data is updated since it was published in our 2022 outlook two weeks ago. As you can see, the average drawdown within the S&P 500 is near-bear market territory (-19%); while it’s much more dramatic within the NASDAQ and Russell 2000 (-42% and -38%, respectively).

Muted Index-Level Drawdowns Belie Massive Churn Under Surface

Source: Charles Schwab, Bloomberg, as of 12/10/2021. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

The nature of these rotational corrections is that pockets of weakness have been simultaneously offset by pockets of strength, which have kept index-level drawdowns more subdued. Indeed, in the case of the NASDAQ, most investors would probably prefer to have a -42% average member drawdown—but an index-level maximum drawdown of only -11%—rather than having the bottom fall out all at once with a 42% drop. This more benign scenario of weakness hasn’t kept investor sentiment from swinging sharply throughout the year, however.

Seesaw of smart money vs. dumb money

One of the most popular sentiment metrics I share from time to time is a daily measure constructed by SentimenTrader (ST), shown below. The labels of Smart Money and Dumb Money Confidence are theirs; and represent real money behavioral (not survey-based/attitudinal) measures of each cohort’s positions. In general, throughout the history of these confidence measures, Smart Money Confidence is the non-contrarian indicator, while Dumb Money Confidence is the contrarian indicator—typically when they’re at extremes.

Smart/Dumb Money Confidence Divergences/Convergences

Source: Charles Schwab, SentimenTrader, as of 12/10/2021. SentimenTrader's Smart Money Confidence and Dumb Money Confidence Indexes are used to see what the “good” market timers are doing with their money compared to what the “bad” market timers are doing and are presented on a scale of 0% to 100%. When the Smart Money Confidence Index is at 100%, it means that those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. The Dumb Money Confidence Index works in the opposite manner.

Admittedly, during the latter part of 2020 and early part of 2021, the “dumb money” was not so dumb—being optimistically-positioned in a sharply rising stock market—while the “smart money” didn’t start to give up its bearish leanings until mid-year. More interesting perhaps is the dramatic flip-flopping that’s been underway since early November.

A continued wide spread, with “smart money” elevated and “dumb money” much lower, would be a positive for stocks near-term based on history. However, if the market’s recent surge back to all-time highs persists, causing a significant retreat in “smart money” positioning alongside a significant acceleration in “dumb money” positioning, it could set the stage for another bout of volatility. A more likely scenario for now is more churn, and more sentiment volatility.

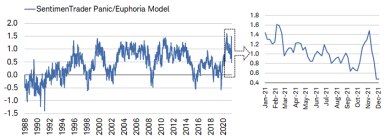

Less euphoria, but no sign of panic

Another sentiment metric showing less euphoria is ST’s Panic/Euphoria Model. This is ST’s take on the very popular Citi Panic/Euphoria Model which was created by my friend and Citi’s Chief U.S. Equity Strategist, the late-great Tobias Levkovich. As the right-side call-out chart below shows, there was a quick move up to euphoric territory heading into “bleak Friday,” but an equally quick move back down, courtesy of the aforementioned 4.4% S&P 500 drawdown in September. It remains in elevated territory, which bears watching, but well down from the record-high level of mid-February this year.

Less Euphoria, But Nothing Resembling Panic

Source: Charles Schwab, SentimenTrader, as of 12/10/2021. This model is based on the Citi Panic / Euphoria model that is published in Barron's magazine. It is composed of the following primary inputs: NYSE short interest, margin debt, Nasdaq vs NYSE volume, Investor's Intelligence survey, AAII survey, retail money market funds, put/call ratios, commodities prices, and retail gasoline prices. The higher the model, the more investors are in a euphoric mood, with lower expected stock returns going forward. Low values, particularly below zero, suggest that investors have panicked and higher forward returns are expected. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

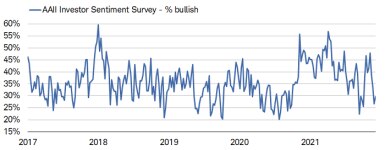

Bullishness has also come way down in the weekly sentiment survey done by the American Association of Individual Investors (AAII), as shown below. This is not to suggest a sentiment measure like this should be viewed through a technician’s lens, but it is interesting that this year has generally seen a series of lower highs and lower lows; or, in other words, has maintained a downward-sloping trend. The larger-than-usual swings could also be explained by the aforementioned significant churn (in terms of stock-level drawdowns) that’s been evident all year.

AAII’s Bulls in Hibernation?

Source: Charles Schwab, Bloomberg, as of 12/9/2021.

Short duration breadth indicator reversed higher

As we wrote in our mid-November sentiment report, sentiment can get stretched into euphoric territory; but if market breadth is healthy, that typically serves as a positive offset. As of last Thursday, the percentage of S&P 500 members trading above their 10-day moving averages was nearly 90%, which was way up from only 5% only five trading sessions prior to that. According to ST data, that is the quickest reversal since last October. ST has looked at similar periods when the percentage of stocks above the 10-day average cycles from oversold to overbought in a short period of time. Their proprietary signal triggered 52 other times in the past 93 years, and subsequent returns and win rates were solid across most time frames; especially out two months.

Diversification/rebalancing key disciplines in this environment

Throughout this year, we have been consistent regarding our advice as to how investors should navigate the churn under the surface of otherwise-mild index-level weakness. An obvious discipline to keep front-and-center is diversification—across and within equity asset classes. Trying to time these swings and flip-flops in advance and positioning accordingly is a fool’s errand. Instead, we have been pressing the benefits of volatility- or portfolio-based rebalancing vs. calendar-based rebalancing—in the interest of trimming into strength and adding into weakness as it’s occurring. It’s a better way for portfolios to stay “in balance” (in line with strategic asset allocation targets) than trying to time the swings in advance.

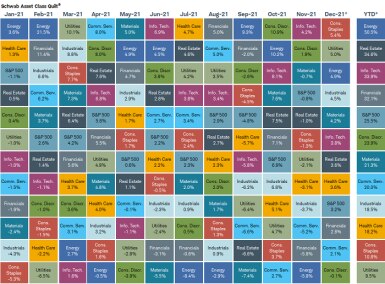

We have also been suggesting investors—specifically of the stock picking variety—take more of a factor-based approach relative to a sector-based approach. An update to our popular “sector quilt” is shown below. It highlights that while there are clear sector winners and losers year-to-date (final column), the variability of those returns on a month-to-month basis are quite extreme. Case in point: Energy is the best-performing sector YTD; however, it’s spent more months as the worst-performing sector (April, July, August and November) than as the best-performing sector (January, February and September).

Source: Charles Schwab, Bloomberg, as of *12/10/2021. Sector performance is represented by price returns of the following 11 GICS sector indices: Consumer Discretionary Sector, Consumer Staples Sector, Energy Sector, Financials Sector, Health Care Sector, Industrials Sector, Information Technology Sector, Materials Sector, Real Estate Sector, Communication Services Sector, and Utilities Sector. Returns of the broad market are represented by the S&P 500. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Returns assume reinvestment of dividends, interest, and capital gains. Past performance is no guarantee of future results.

In the midst of these rapid-fire sector rotations, quality-based factors have been more consistent outperformers. The early part of 2021 was characterized by lower quality outperformers—including factors like non-profitability. The chart below looks at four popular indexes that have become “poster children” for highly-speculative, lower-quality market segments. The non-profitable tech and most-shorted indexes are self-explanatory, but have more detail within the footnotes. The ISPAC index tracks newer Special Purpose Acquisition Companies (SPACs); while the retail sentiment index tracks the stocks that are the most popular/most mentioned on Reddit’s Wall Street Bets page (through which meme stocks initially got their popularity).

Spec Areas’ Volatility and Drawdowns

Source: Charles Schwab, Bloomberg, as of 12/10/2021. Goldman Sachs (GS) non-profitable tech basket consists of non-profitable U.S.-listed companies in innovative industries. Technology is defined quite broadly to include new economy companies across GICS industry groupings. GS most-shorted basket contains the 50 highest short interest names in the Russell 3000; names have a market cap greater than $1 billion. GS retail sentiment basket consists of U.S.-listed equities that are most popularly mentioned and discussed on Reddit's r/WallStreetBets page. ISPAC Index is a passive rules-based index that tracks the performance of the newly listed Special Purpose Acquisitions Corporations (SPACs) ex- warrant and initial public offerings derived from SPACs since 8/1/2017. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

One quality-based trend that we see persisting can be illuminated by looking at the blue line above, which represents non-profitable tech stocks. As the economic cycle continues to mature—bringing along high inflation and tighter monetary policy by the Federal Reserve, lower-quality companies with weak (or no) profitability will likely continue to underperform.

At the factor level (using Cornerstone Macro’s factor screening tools), you can see below the steadily increasing improvement in the “revisions ratio” factor (favoring stocks with steadily-rising earnings revisions). This is particularly important as we head into 2022, which is expected to be a more challenging year for corporate earnings. Conversely, since September’s market weakness ended, the “negative earnings” factor has been in retreat and sits firmly in negative territory.

Positive Earnings Revisions Besting Negative Earnings

Source: Charles Schwab, Cornerstone Macro, as of 12/10/2021. Factors based on sector-neutral S&P 500. Factors shown highlight stocks with stronger upward revisions to earnings growth and stocks with no net income on a trailing 12-month basis. Past performance is no guarantee of future results.

Other factors (or characteristics) that continue to look attractive given where we are in the economic and monetary policy cycle are strong free cash flow, strong balance sheets, and low debt-to-equity ratios. The one sector that generally incorporates many of these quality-based factors is Healthcare—which is currently the only sector on which Schwab has an “outperform” rating (see more on Schwab.com from our sector guru, David Kastner). This by no means suggests the sector will be a consistent performer (or will have all its members performing well with any consistency), so do your research at the individual stock level.

In sum

This year has been a strong one for most major stock market averages; but with ample churn and sector volatility under the surface. Instead of trying to get ahead of these short-term swings, use them to your advantage via diversification, but also volatility/portfolio-based rebalancing in the interest of trimming into strength and adding into weakness. Keep a close eye on sentiment conditions, especially if they move back toward euphoria—and if not accompanied by breadth improvement. As I often say, it’s not what we as investors know (about the future) that matters, but what we do along the way.