Market Volatility: What If You Don’t Have Time to Recover?

By

By

It’s one thing to stick to a long-term investment strategy in a good market—or in a down market, if you have time to recover. But what if you don’t? What if your time horizon is short or you have a goal with a series of time frames, like a multi-year retirement?

If you’re investing for a long-term goal, a combination of time in the market, consistent contributions and a long-term strategy works. However, if you’re investing for a short time frame, short-term volatility is your enemy. As economist John Maynard Keynes famously said, “Markets can remain irrational longer than you can remain solvent.” Don’t fall into this trap when creating your investment strategy.

What is a "short" time horizon?

For the average investor, a short time horizon doesn’t mean a day or a week. A short time horizon, more realistically, is four years or less. If you expect to need the money within that time frame, you shouldn’t be invested aggressively, unless you can afford to lose money and still meet your goals. That’s the nature of investing.

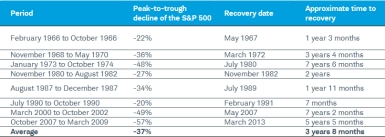

Why four years? Since the 1960s, the average time from the peak in an up market to the trough in a down market and back up again has been about three and a half years. Future downturns could be longer or shorter, but a four-year time horizon is a cushion that can help manage risk in most markets.

Historical peak-to-trough-to-peak time periods for the S&P 500® Index

Note: Time period uses 30/360 day count convention, and is only expressed in months.

Source: Schwab Center for Financial Research with data provided by Bloomberg. Chart reflects periods in which the S&P 500 Index fell 20% or more over a period of at least three months. Time to recovery is the length of time it took the S&P 500 to complete its peak-to-trough decline and then rise to its prior peak. Past performance does not guarantee future results.

Prepare for market volatility before it happens

Your first line of defense against market volatility is a portfolio that is appropriately allocated based on your goals and investing timeline. We often talk about having a long-term strategic asset allocation, but that generally makes sense only if you have a long-term investment objective. Most investors have multiple investment goals, with different time horizons, which can be used to build investment plans and then portfolios. And for each one, you should build your asset allocation based on the date you expect to need the money.

At Schwab, the first of our investing principles is to establish a financial plan based on your goals and investing timeframe. Then identify an investment allocation suited to each goal (if you need help, start with Schwab’s Investor Profile Questionnaire or talk with a Schwab Financial Consultant to help with an investment strategy for each of your investment accounts and goals). As a rule of thumb:

- For shorter-term goals, a sound approach is to invest in a heavier mix of historically less-volatile investments, such as cash investments and short-term bonds.

- For intermediate-term goals, a diversified portfolio including cash investments, bonds and some stocks can help to balance your risk and return potential. The closer you are to your goal, reduce your risk accordingly.

- For longer-term goals, where you have the capacity to weather a few down days or even a bear market, you can invest more aggressively.

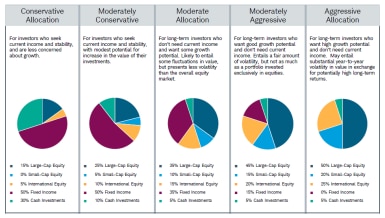

The illustration below shows Schwab sample portfolios based on risk tolerance. When your time horizon is four years or more, it has made sense, historically, to take greater investment risk—for example, you might consider the “moderate,” “moderately aggressive” or “aggressive” allocations shown below. On the other hand, if you have a shorter time horizon, a portfolio weighted toward more-stable assets—such as cash investments, certificates of deposit or U.S. Treasury bills—is usually a good idea (consider the “conservative” or “moderately conservative” allocations shown below).

These sample portfolios illustrate various potential allocations based on risk tolerance

Source: Schwab Center for Financial Research. For illustrative purposes only. Portfolios managed at Schwab may vary, or may have more detail, asset classes or investments, depending on how you work with Schwab.

What if you’re approaching retirement or already there?

Portfolios for investors near or in retirement are unique: They have not one, but several time horizons: now (money you’ll need in the next year), soon (money you’ll need during the next two to four years) and later (money you’ll need more than four years from now, for a long, but indefinite, period of time). Few investors cash out their entire retirement portfolio all at once.

Portfolios for people near or in retirement should include a mix of investments to fund spending now, soon and later. Beyond simply being diversified, these portfolios should contain an appropriate combination of higher- and lower-risk investments.

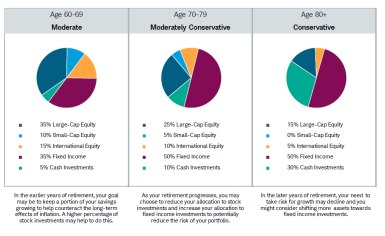

The chart below shows Schwab’s sample portfolios for retirement, for those who plan to spend from their portfolios. Remember, you’re not going to spend it all at once, but over a period that could last 30 years. You should target an allocation that combines low-risk investments for the shorter term and investments with higher return potential for the longer term, and you may choose to shift to a more conservative allocation as you move through retirement. Ideally, the lower volatility potential in these portfolios can reduce the risk of your not having money from investments when you need it.

Sample allocations for investors in retirement

Source: Schwab Center for Financial Research. For illustrative purposes only. Portfolios managed at Schwab may vary, or may have more detail, asset classes or investments, depending on how you work with Schwab. Although it’s generally recommended that you shift to a more conservative investing approach during retirement, your asset allocation depends on your own circumstances and tolerance for risk.

When we think of risk when investing, short-term volatility is typically the risk we mean. When we think of risk in retirement, a better definition is: not having enough money when you need it. In building a retirement portfolio, you should target the appropriate amount of risk in different buckets to meet your “now,” “soon” and “later” needs.

What if you didn’t plan?

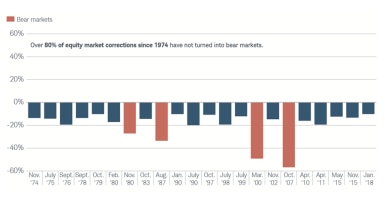

If the market is dropping before you had a chance to prepare, don’t panic. Take the time to reconsider your goals, with time horizon, and risk tolerance. Even if a down market feels uncomfortable, remember that most market downturns are relatively short. Historically, only a few stock market corrections have turned into bear markets—and that takes into account only downturns that were fairly substantial to begin with, at 10% or more. It can be unnerving when the market is down sharply, but before you take any action, it’s useful to put the downturn in perspective.

Since 1974, only four of 22 market corrections have turned into bear markets

Source: Schwab Center for Financial Research with data provided by Morningstar, Inc. Each period listed represents the beginning month/year of either a market correction or a bear market. Corrections are defined as a decline of more than 10%, but less than 20%. Bear markets have declines greater than 20%. The market is represented by the S&P 500® Index. Past performance does not indicate future results.

Also, if you have a longer time horizon, market drops and even bear markets can be an opportunity to buy shares at lower prices. When markets or sectors of the market fall in price, it can be an opportunity to purchase more shares for the same dollar invested, in a diversified investment exposed to that market sector, such as a diversified mutual fund or exchange-traded fund. Buying when investments are less expensive and selling when they are more expensive can boost long-term wealth over time.

If you didn’t plan for a down market, and have a short time horizon, consider alternatives to selling during a down market. This is where having a year’s worth of expenses in cash, plus a short-term reserve, can really help—if you have the resources to wait out the volatility or bear market and not sell more volatile investments, you’ll be better off. If you don’t have other income or investments that have held or risen in value, ask yourself if there’s any way you can avoid selling investments at depressed prices. Do you have other sources of income you could tap instead? Can you reduce your spending? If you can, it can prolong the life of your portfolio considerably.

What can I do now?

After reviewing each of the points above, you may want to talk with a Schwab Financial Consultant to review your financial and investment goals and investment strategy and time horizon for each. A Financial Consultant can help with a financial plan, or can point you to solutions and advice that take into account your specific circumstances and goals. This should help you feel more comfortable investing in both good and bad markets, based on your goals, not market volatility or even a bear market.